Long and Good

05 July 2023

Bond prices fall when interest rates rise. If I'm holding a bond A paying 3% a year, and tomorrow a bond B comes out paying 4% a year, the price of bond A has to fall for the 3% to represent a 4% return on the new price.

The longer the bond's maturity, the stronger this effect. To give an example, a holder of a ten-year bond issued by France's largest capitalization -LVMH- lost 20% in 2022 when yields rose to 3%.

Despite what the central bankers were saying, we could still imagine that, with rates at their all-time lows, the risk of them rising was not zero. In fact, the risk was much greater after the massive injections of liquidity to counter COVID.

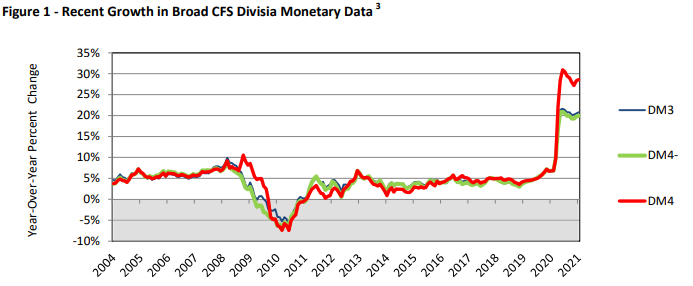

Below you can see the evolution of money supply published by the Center For Financial Stability at the beginning of 2021.

This graph represents the money supply. Schematically, if the quantity of money in the system increases faster than the quantity of goods/services, prices rise. The title of their year-end publication was "Get ready, mass inflation is coming". As an investor, now is not the time to own long-term bonds. Those who had them suffered in 2022.

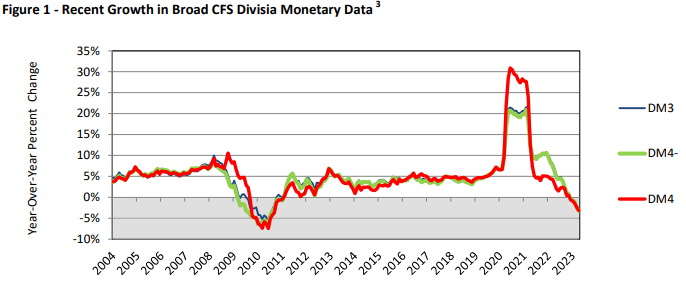

Here's the same graph with today's data:

Their message today: "Central banks don't realize they're squeezing too hard."

If the trend on this graph is the opposite of the previous one, this argues in favor of lower prices.

A tight squeeze means recession, less demand and lower prices.

It's anything except an exact science, but I don't see many scenarios with much higher inflation. So long-term rates shouldn't rise much further. And above all, as soon as inflation signals calm down, central banks will try to lower their rates. For as Raghuram Rajan (the only IMF economist to have predicted the subprime bubble) said: "If as a central banker you don't cut rates when inflation is under control, you will be suspected of not applying a stimulus to the economy that could be."

So it's time to take a serious look at adding long-term bonds to portfolios, but beware: you'll have to be extremely selective. Long rates may not rise much further, but just if they stay there, there are a number of companies that were holding out with zero rates and will disappear with 3% rates.

So, long and good, that's what you have to look for.

Disclaimer

This presentation is a promotional document. The content of this document is communicated by and is the property of Monocle Asset Management. Monocle Asset Management is a portfolio management company approved by the Autorité des Marchés Financiers under number GP-20000040 and registered with the ORIAS as an insurance broker under number 10058146. No information contained in this document should be construed as having any contractual value. This document is produced for information purposes only. The prospects mentioned are subject to change and do not constitute a commitment or a guarantee. Access to the products and services presented here may be subject to restrictions for certain persons or countries. Tax treatment depends on individual circumstances. The fund mentioned in this document (Monocle Fund SICAV) is authorized for marketing in France and possibly in other countries where the law permits. Before making any investment, it is advisable to check whether the investor is legally entitled to subscribe to the fund. The risks, costs and recommended investment period of the funds presented are described in the KIDD (key investor information documents) and the prospectus, available free of charge from Monocle Asset Management and on the website. The KIDD must be given to the subscribers before the subscription. Past performances are not a reliable indicator of future performances. Monocle Asset Management cannot be held responsible for any decision taken or not taken on the basis of information contained in this document, nor for the use that could be made by a third party. The investor may lose all or part of the amount of capital invested, as the funds are not capital guaranteed.

To unsubscribe or for any information request, you can email us at monocle@monocle.lu