Risk and the bubble

01 March 2024

The best way to avoid risk is to face it head-on.

The risk for Nvidia is a valuation bubble following the emergence of Artificial Intelligence.

First of all, there have always been valuation bubbles behind technological revolutions. I highly recommend the book "Engines that move markets" by Alasdair Nairn, which tells these stories. Electricity, cars, trains, the internet... every time there's a major innovation, two things happen: yes, the world changes, and yes, a number of investors get wiped out.

So with Nvidia's market capitalisation at $1.900bn today, it's wise to ask yourself this question. And you have to ask it either as a Nvidia shareholder, or just as an active manager: this stock and the six megacaps that go with it have become the market, so it would be wrong to ignore it. "Became the market" is illustrated by this chart showing the correlation between the normal S&P500 (weighted by capitalisation) and the S&P500 Equal Weighted (each of the 500 weighs the same in the index).

This correlation has always been around 1 except at four periods in history: the bubble of 2000, the volatility bubble before Volmageddon in February 2018, the Everything Bubble of 2021 and ... today.

This means that, on the one hand, we are in a special moment, and on the other hand, we all have the S&P500 index as a benchmark, and that this index boils down to these megacaps on which we need to have an opinion.

Sur ces 7 valeurs – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia et Tesla – c’est Nvidia, à +60% depuis le début de l’année, qui mène le bal en 2024. A ce niveau de valorisation, si vous voulez faire du 10% de rendement sur les 10 prochaines années – pas la lune – en investissant aujourd’hui dans Nvidia, cela veut dire que vous visez une capitalisation de $5.000Mds. A 25x de PE, cela veut dire que votre objectif de résultat pour Nvidia dans dix ans, c’est $200Mds de résultat net. Pas impossible, mais pas une paille.

1/ 50%+ operating margin is impressive, and it whets the appetite. All Nvidia's competitors are salivating over their design offices to get their piece of the pie.

2/ Nvidia is B-to-B: its customers are companies. They are not individuals - like Apple or LVMH. When your customers are companies, it's harder to create a monopoly. Price will always be a factor.

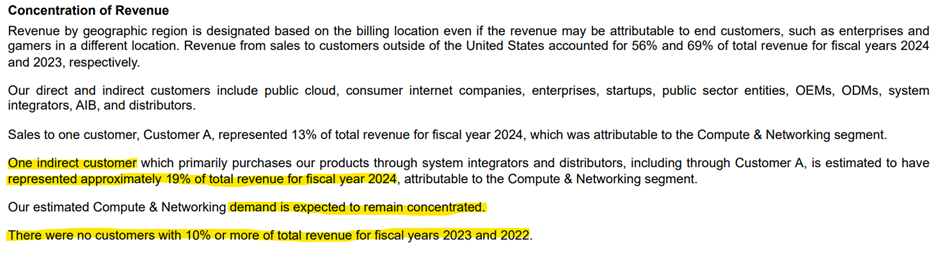

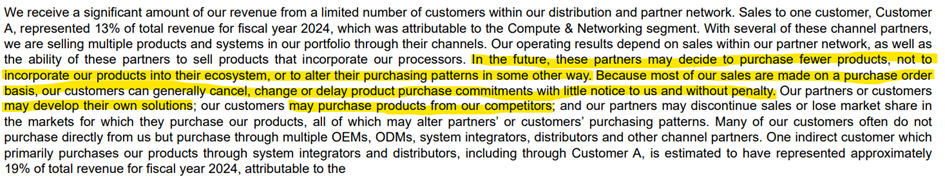

3/ And Nvidia's customers are the biggest Bs in the world. In its annual report (the '10 K' published last week, see below), Nvidia explains that its biggest customer in 2023 (fiscal year 2024) will account for 19% of sales.

The top four must account for almost 50% of sales, and their names are META, AMAZON, GOOGLE and MICROSOFT. Is this a risk for Nvidia? We can look at the problem from this angle: 4 guys account for half of your sales. These sales represent Capex for them. If they decide to cut back, a large part of your turnover will suddenly disappear. And it's possible/probable that if one cuts back, all will cut back and at the same time it will probably be a question of weather - recession. And given the size of these customers, there are no replacements on the bench. The 'Customer A' referred to by Nvidia in its 10K at 19% of sales represents $12bn. Here are the 2023 Capex figures for the quartet:

Microsoft $35 Mds

Alphabet $32 Mds

Meta $27 Mds

Amazon (partie AWS) $25 Mds

So these figures show that if Client A leaves, it will be difficult to find a plan B.

All this is obviously recognised by Nvidia in its risks (see below). But is it really recognised by the market?

The problem with depending on your customers' investment cycles is that these cycles can change.

Let's look at the 2000s - same kind of valuation, same problem of concentration on a few names as seen above.

The names comparable to Nvidia at the time were Cisco, Oracle and Sun Microsystems, three tech companies in the B-to-B sector and among the biggest US market capitalisations at the time.

Sales in 1997, 1998, 1999 and 2000 were +57%, +32%, +43% and +55% for Cisco. For Oracle +35%, +26%, +24%, +15%. The same kind of figures for Sun.

But nothing happened for the next three years. In 2003, both companies had lower sales than in 2000. This was not dramatic for the companies. They continued to operate and to make profits. But it was dramatic for the stocks: Cisco lost 80% and never recovered. Oracle lost 70% and took fifteen years to get back to zero. Sun lost more like 90%. I re-read Sun's 10K for 2000. Do you know what it shows? A Customer A at 19% - General Electric was the customer.

And this sentence:

« Our business could be adversely affected if this customer or another significant customer terminated its business relationship with us or significantly reduced the amount of business it did with us. »

« Our business could be adversely affected if this customer or another significant customer terminated its business relationship with us or significantly reduced the amount of business it did with us. »

Market and portfolio focus

Behaviour:

From 16/02 to 23/02, the fund lost 0.3%, the CAC 40 gained 2.6% and the S&P 500 1.7%. Galapagos was the main negative contributor, costing us 0.5%. On the positive side, Tidewater was the best contributor (+0.3%).

Lines:

This week we exited LVMH, which had rebounded well since our entry at the beginning of the year. We also reduced our exposure to Dollar General to below 5% and initiated a new line with Alphabet at 5%, taking advantage of the poor reception of Gemini, its competitor to ChatGPT.

Have a good weekend,

Charles

Disclaimer

This presentation is a promotional document. The content of this document is communicated by and is the property of Monocle Asset Management. Monocle Asset Management is a portfolio management company approved by the Autorité des Marchés Financiers under number GP-20000040 and registered with the ORIAS as an insurance broker under number 10058146. No information contained in this document should be construed as having any contractual value. This document is produced for information purposes only. The prospects mentioned are subject to change and do not constitute a commitment or a guarantee. Access to the products and services presented here may be subject to restrictions for certain persons or countries. Tax treatment depends on individual circumstances. The fund mentioned in this document (Monocle Fund SICAV) is authorized for marketing in France and possibly in other countries where the law permits. Before making any investment, it is advisable to check whether the investor is legally entitled to subscribe to the fund. The risks, costs and recommended investment period of the funds presented are described in the KIDD (key investor information documents) and the prospectus, available free of charge from Monocle Asset Management and on the website. The KIDD must be given to the subscribers before the subscription. Past performances are not a reliable indicator of future performances. Monocle Asset Management cannot be held responsible for any decision taken or not taken on the basis of information contained in this document, nor for the use that could be made by a third party. The investor may lose all or part of the amount of capital invested, as the funds are not capital guaranteed.

To unsubscribe or for any information request, you can email us at monocle@monocle.lu